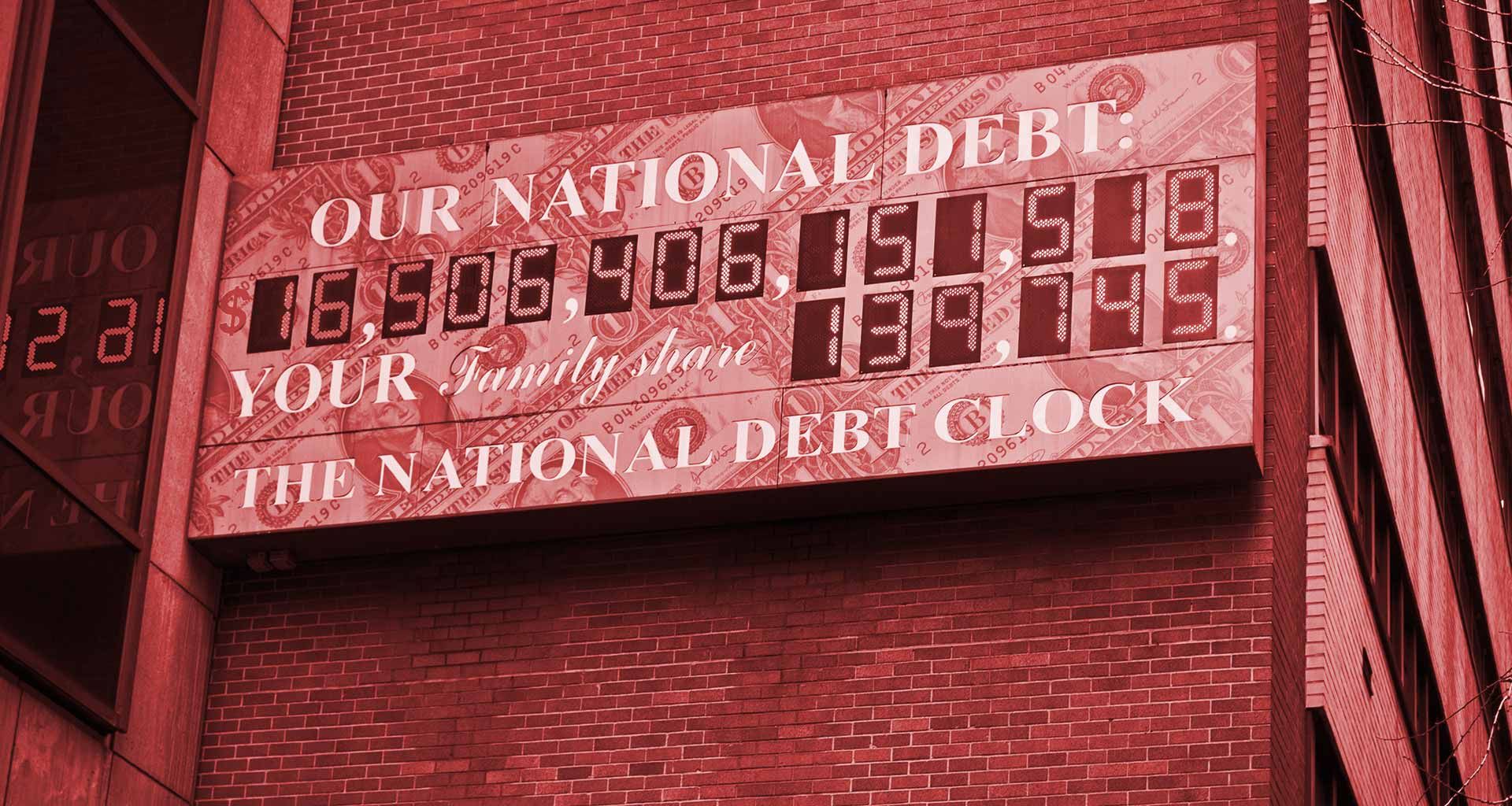

The U.S. national debt is rising by $1 trillion roughly every 100 days right now, which now stands at nearly $35.8 trillion as of 10/22/2024. To make matters worse, the Treasury has also drawn down its cash balance by $72 billion putting it over $275 billion in the red.

The report spread like wildfire, especially throughout the financial and entrepreneurial communities. Tesla CEO Elon Musk was prominent among those, saying, “If there is not radical reduction of government expenditures, then, just like an individual who has taken on too much debt, America will become de facto bankrupt.”

Currently, the ratio of federal debt to GDP, which is a critical metric for assessing fiscal health, is expected to rise from approximately 99% in 2024 to about 116% by 2034. As a result, the U.S. budget deficit has grown to $1.833 trillion for fiscal year 2024, the highest ever outside of the pandemic era. Financial experts are understandably concerned because we are facing unprecedented economic conditions. The consensus is that there’s a tremendous risk to long-term sustainability as interest costs tied to mandatory spending continue to grow faster than tax revenue.

To put this in perspective, the maximum debt to income lenders will accept is 43% but most prefer to see a more reasonable cap of 36%. If you own a home, I want you to think back to what the application process was like, and then imagine trying to convince your lender to approve a mortgage payment that is 16% more than you make. That’s where we are as a nation. It’s ridiculous, embarrassing, and quite frankly, catastrophic.

Unfortunately, because of a severe lack of financial literacy in this country, most people are not only unaware that we’re in this position, but they also wouldn’t understand the significance if they knew about it. A recent study from MarketWatch found that nearly half of Americans don’t understand basic financial concepts, which also explains why according to a Georgetown University study, about 55% of Americans between the age of 55–64 had less than $25,000 in retirement savings and 41 percent had absolutely nothing saved, and the Federal Reserve Bank of New York reported that consumer debt is at historic levels.

So what does this mean, both for America as a nation and each of us individually?

Well, as a nation, without implementing some pretty significant austerity measures very soon, our economy will begin to decline and we will lose authority as a world leader. This has been happening for decades, but the speed has been increasing dramatically in recent years. From an economic standpoint, we’ve all seen the impact of this with the runaway inflation that has wreaked havoc on Americans across the country. And from a geopolitical standpoint, BRICS is a growing movement that threatens our status as a superpower. This is critical because that status is the foundation of our economy since President Richard Nixon took our economy off the gold standard and essentially replaced it with the equivalent of, “Just trust me.” The U.S. switched to a fiat money system. This is what’s called fiat money, which has no value of its own and doesn’t represent anything of value, such as gold, but our government declares what it’s worth. Without our position as the world’s superpower, this declaration becomes meaningless because we no longer have enough geopolitical clout.

This leads to hyperinflation, and eventually economic collapse, similar to what we saw in Venezuela. As the value of our dollar plunges, everything becomes less affordable, and we can no longer rely on imported products anymore because they will become cost prohibitive. Unfortunately, there’s another side to this problem, which is that we lack the necessary manufacturing capacity to produce what we need locally. That will create significant supply chain challenges that can make it incredibly difficult to run a business, which then causes more job losses down the road.

The solution here is to make drastic cuts to government spending, which includes completely eliminating many government entities, which can offer a side benefit of helping businesses become more profitable by reducing burdensome and costly regulations. This is critical because small businesses are the backbone of our economy and employ about half of the US workforce.

As an individual, we all need to become more financially resilient by improving our financial literacy, reducing expenses, and creating additional revenue streams.

Financial literacy is the foundation, and it’s something most Americans are missing. Fortunately, there are a lot of organizations that are making this a priority. For example, just a few years ago, the DeSantis administration signed a law that mandated the Florida Department of Education to include financial literacy education in all Florida schools. My team has been teaching the children of our Freedom Founders members financial literacy through NexGen. And recently, a Florida high school teacher and coach, Eric Scrivens, launched an organization with a mission of placing free financial literacy libraries all over the country.

I think a large part of why more people are focusing on this than ever before is because of how the economy has been going. When people can’t afford to live, they tend to start looking for answers as to why, followed by a search for solutions.

This is great because once someone learns how finances work, they can leverage that knowledge for the rest of their lives to create a better future for themselves and their families. More importantly, this education empowers them to demand better fiscal policy from lawmakers.

America is at a turning point, and it’s up to every one of us to financially, both do better ourselves, and demand better from our elected representatives.